Managing the Unmanageable: Historical Playbooks for National Debt Reduction

Notes from My Weekly Feed #22: What history tells us about solving high national debt burdens....

Today is a relatively short post that took me relatively longer than usual to research for. It was very fun nonetheless.

We all keep reading and hearing about the looming debt crisis. And I was curious to find out whether Debt-to-GDP were ever historically as high or higher in advanced economies? And if so, how did advanced economies solve for it.

This brief blog is a summary of my research so far.

Please feel free to provide feedback / challenge / disagree any of these points as I strive to learn from y’all in public.

And, if you have not subscribed yet, could you do me a solid and please subscribe :)

Lessons From History - How Have Developed Economies “Worked” Their Way Out of Massive Debt Overhangs

One thing that’s had bipartisan support in the U.S. for decades, perhaps the only thing, is taking on debt. More debt.

The interest rate a country pays on its debt reflects how creditworthy that country is. But as borrowing piles up - the bond market, the same market happily feeding that appetite for debt, starts to get nervous about the borrower’s ability to manage its debt burden. Nervous lenders demand higher returns for taking on more risk, i.e. higher interest rate on new debt.

As interest expense gets higher, countries borrow more just to pay the interest on existing debt.

None of the new borrowing is funding productive investment; it’s simply new debt to pay old debt. Which is why debt-to-GDP ratios are climbing alarmingly across nearly every major economy.

To spell it out (at the risk of sounding repetitive): a rising debt-to-GDP ratio means governments are creating more debt than economic value. The new money being borrowed isn’t generating enough growth to keep up with a government’s financial liabilities.

And this dynamic is starting to spill into politics. Across Europe, taxpayers are rebelling / protesting / rioting against governments trying to rein in spending. A popular meme circulating in several European countries shows “Highly-Taxed Nick” paying into the welfare state — while that state, burdened by an aging and ailing population, keeps asking for more from Nick. In France alone, 5 Prime Ministers have lost their jobs in the last 2 years in their attempt to cut spending on public welfare programs that is largely responsible for rising debt levels in the country.

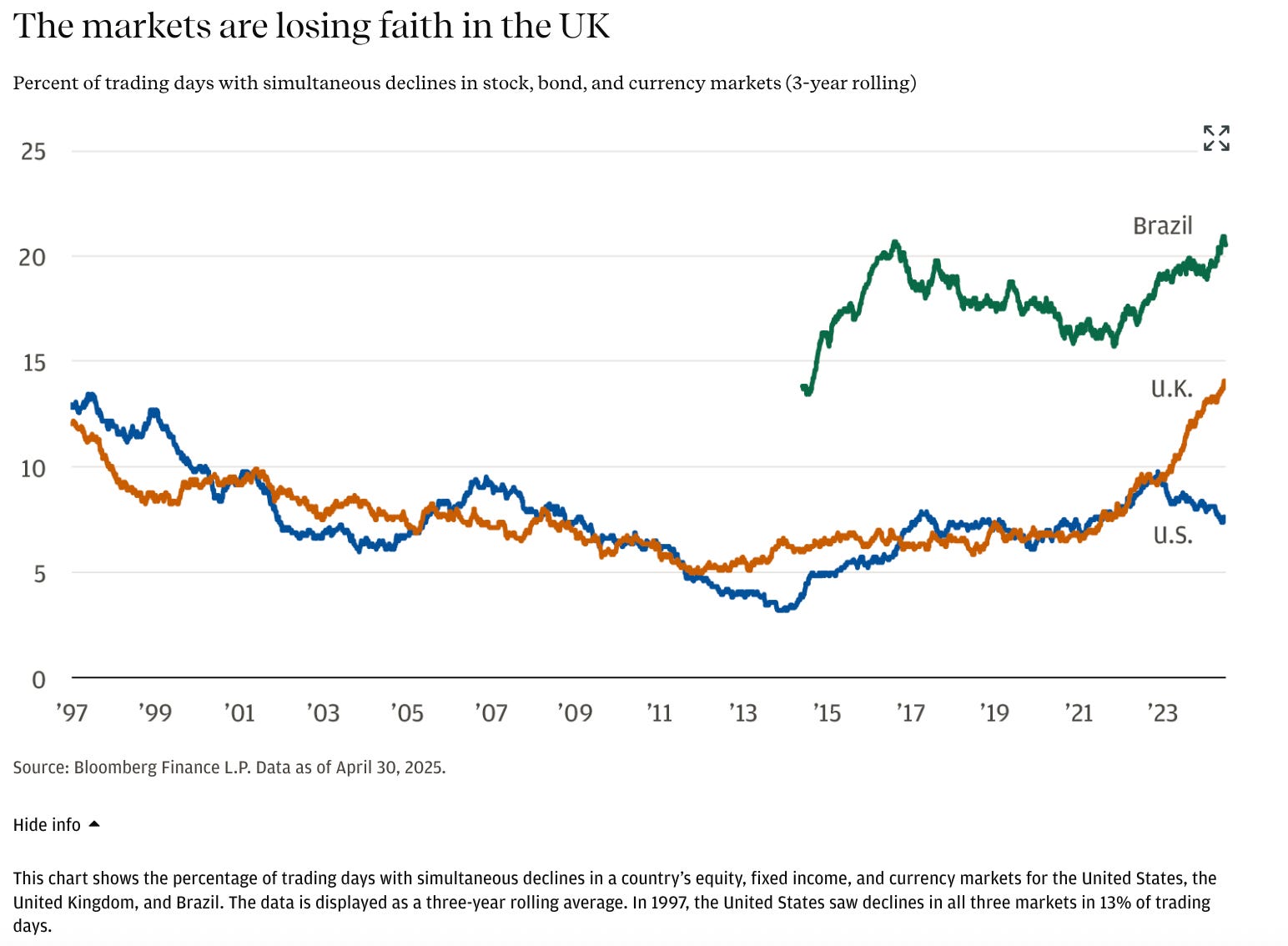

Nowhere is the situation so dire as in the U.K. The bond markets have completely lost their faith in the U.K. government’s ability to either (a) manage its budget “wisely” or (b) its ability to pay its bill in the future. The U.K. may potentially be the first nation I will see in my lifetime that goes from being an advanced economy to an “emerging” economy.

We’ve all read plenty about why this is a big, big problem. I have written about this previously and I’ll probably continue writing more on this later, not as a doomer but just as a curious observer of what I consider a historic moment in human civilization.

But today, inspired by a brief Economist article I wanted to look at something different:

How have countries historically solved the problem of having too much debt?

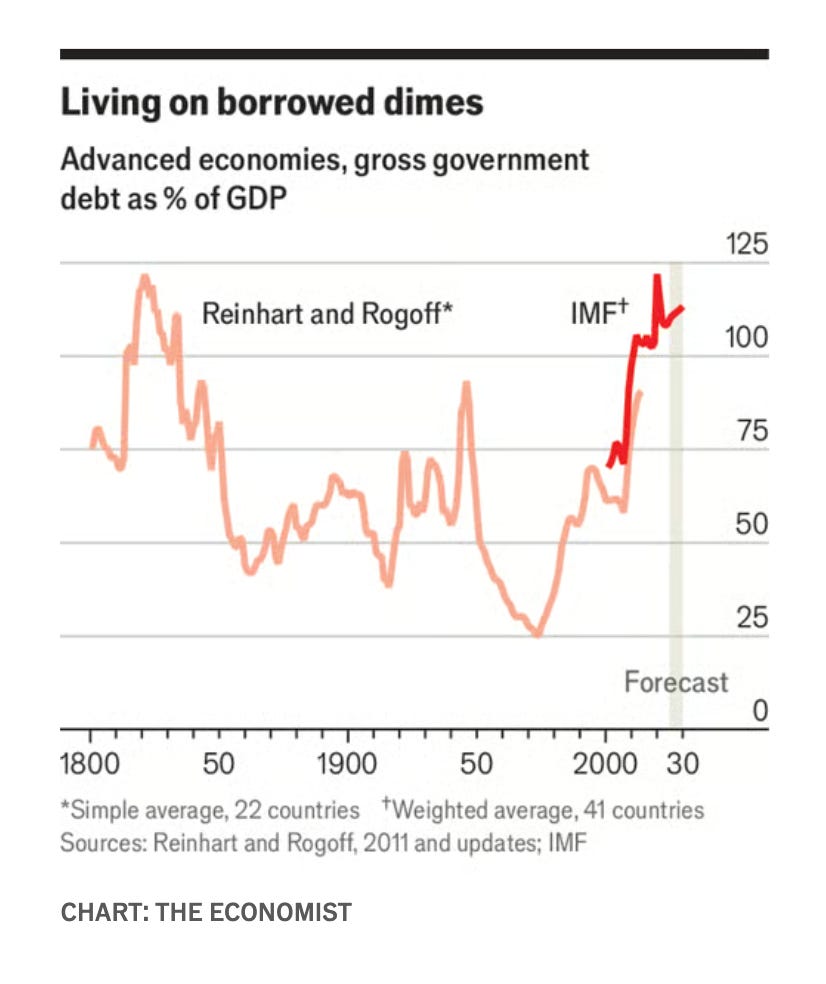

Back in 2015, Carmen Reinhart (Harvard) and M. Belen Sbrancia (IMF) published a fascinating paper on exactly this question: How have nations with dangerously high debt-to-GDP ratios managed to “liquidate” their excess debt and return to normal levels?

The answers aren’t particularly comforting. But hey, we have at least lived through such periods in history and not just survived, but eventually thrived.

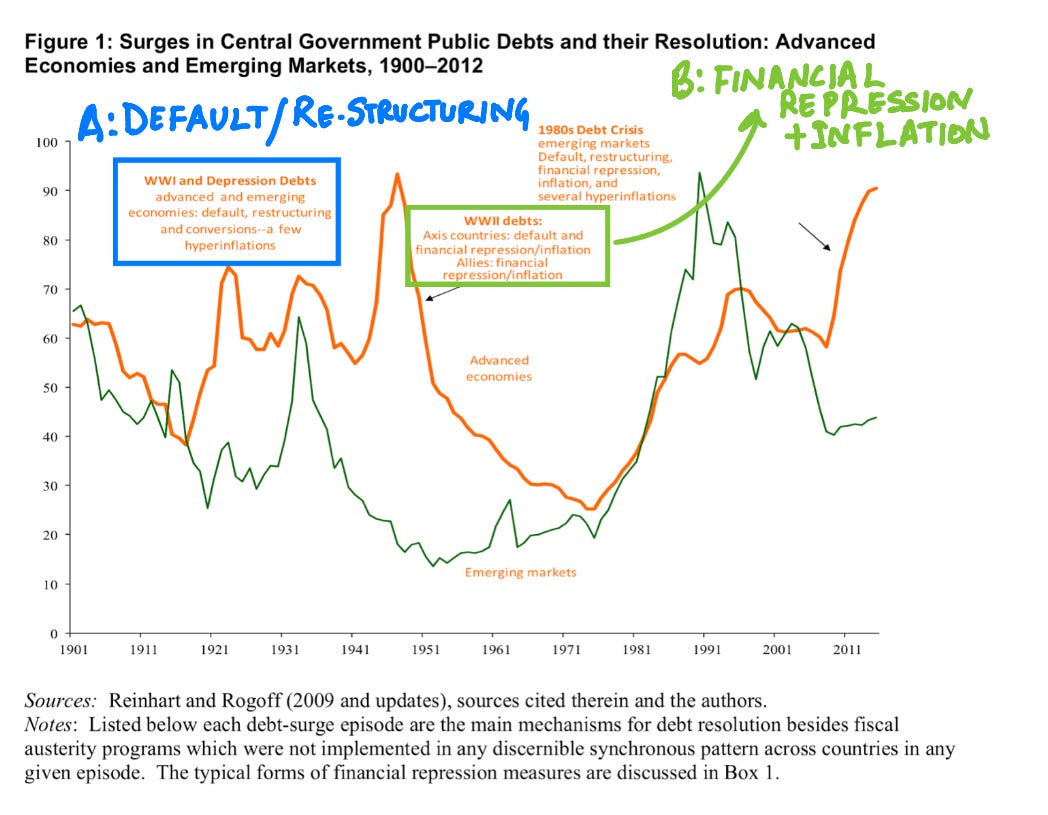

From the chart above, the authors identified two major high-debt eras for advanced economies:

World War I and the Great Depression (1914–1945)

World War II and the postwar reconstruction period (1945–1970s)

The 1980s debt crisis, by contrast, was largely an emerging-market story, driven by unmanageable foreign borrowing. And note that this paper was published in 2015 so amidst the post-2008 and prior to the COVID-related debt boom.

Across these episodes, the authors found two broad ways countries “solved” their debt problems, none of them painless.

A - Default / Restructuring

This was common before World War II, especially during the Great Depression. In simple terms, countries stopped paying what they owed and then renegotiated the terms of their debt to make repayment easier.

Sometimes this meant extending the repayment period or paying back only part of what was due. Advanced economies could do this because their governments controlled the legal and financial systems through which debt was issued, giving them the power to change the rules or force a “re-structuring” of terms if needed. Creditors often had little choice but to accept the new terms, since refusing could mean losing everything if the government chose to default completely.

For example, after World War I, France faced a massive debt overhang and restructured many of its obligations, stretching repayment timelines and lowering interest costs to restore fiscal stability.

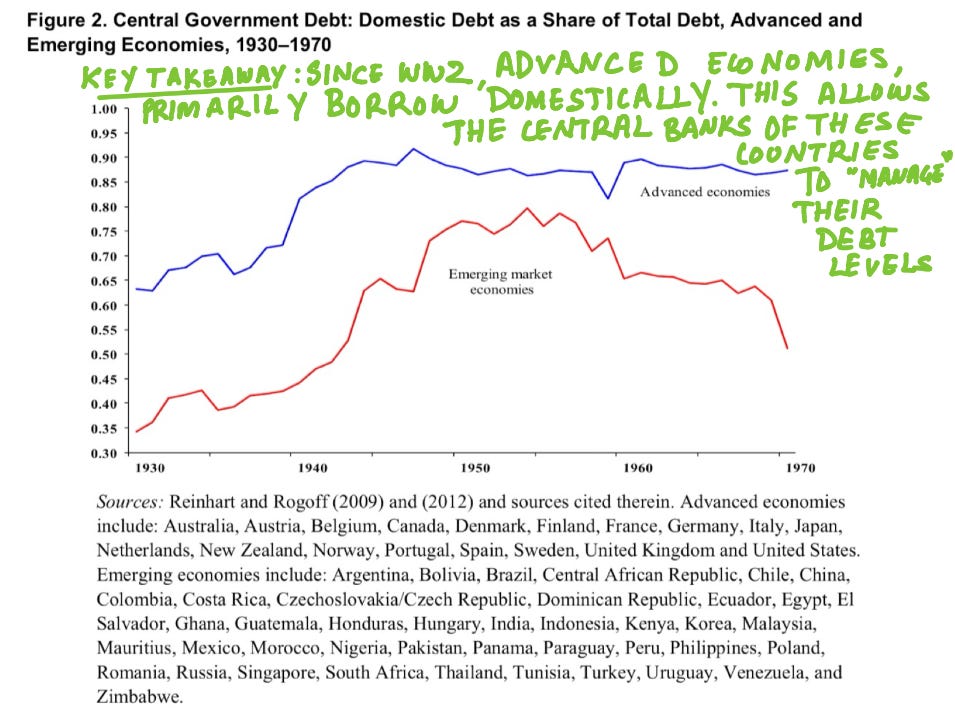

Since World War II, outright default has become rare among advanced economies. One reason why defaults are uncommon is because, after the 1940s, most government debt shifted from foreign to domestic investors, and countries gained the ability to issue debt in their own currencies. That gave them more tools, such as controlled interest rates and inflation, to manage high debt without formally defaulting.

B - Financial Repression and Inflation To Manage High Debt:

After World War II, as defaults became politically and economically unacceptable, most advanced economies relied instead on what the authors call ‘financial repression’ to bring down their debt.

In simple terms, financial repression means using government influence to keep interest rates low and money inside the domestic financial system. Banks and investors were often required — formally or informally — to hold government bonds, while capital controls made it hard for savers to move money abroad. The end result was that governments could borrow cheaply from captivated creditors for long periods of time.

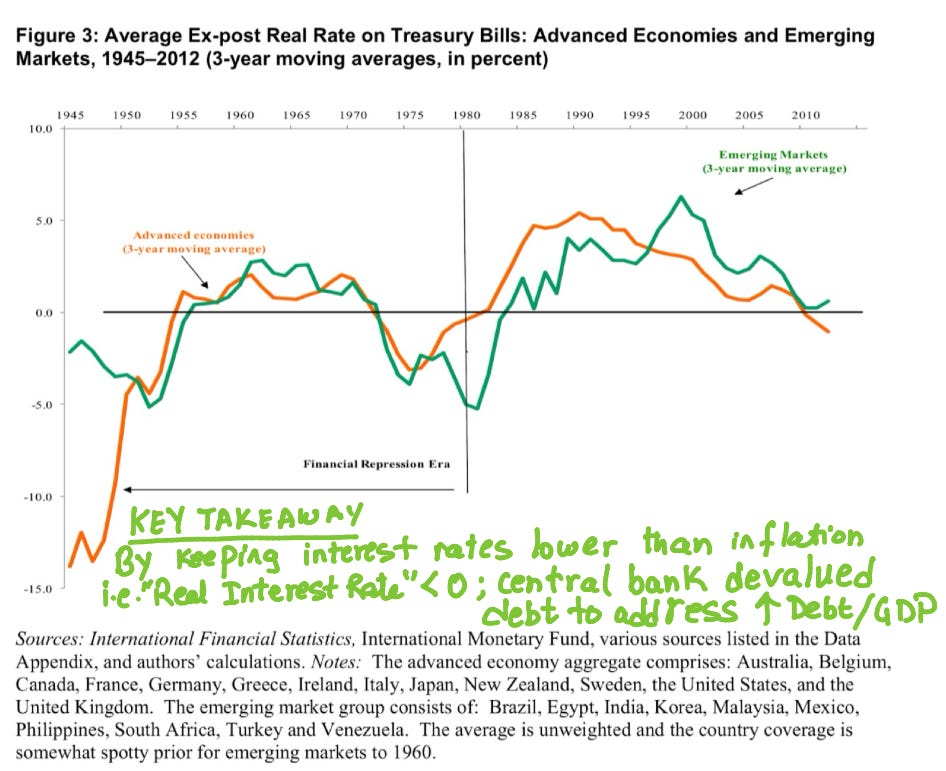

Financial repression often worked hand in hand with inflation. When prices rise across the economy, the value of money, and therefore the real value of existing debt, falls. In other words, the dollars a government owes tomorrow are worth less than the dollars it borrowed today. This acts as a quiet transfer from savers to borrowers, and in this case, the biggest borrower is the government.

Central banks played a key role in this process. By keeping interest rates below the rate of inflation, they helped ensure that the government’s debt lost value in real terms. Over time, even moderate inflation combined with low interest rates eroded a significant share of the debt burden without the government ever having to default or formally restructure its obligations.

While this strategy worked for decades, many — including, most famously, Ray Dalio (Principles for Navigating the Big Debt Crisis)— have warned that it creates a false sense of control. When governments repeatedly use financial engineering to manage debt, it can breed the illusion that borrowing has no limits — that any debt can be made affordable by keeping rates low or letting inflation quietly do the work. Over time, this dulls fiscal discipline and makes economies increasingly dependent on cheap money. But, as Dalio notes, the bill always comes due and when it does, the adjustment is sudden and painful.

C: Good Old Debt Reduction Through Fiscal Austerity or Increased Productivity:

This was not the main focus of the paper, but the authors briefly acknowledge that debt can, in theory, be reduced the “romantic way” — by cutting wasteful spending, running budget surpluses, and creating a regulatory environment that fuels real growth. Think of it as the fiscal equivalent of what Elon Musk recently tried to make happen with DOGE i.e. cut wasteful government spending to tighten budget, reduce deficit and eventually run a budget surplus to pay down debt.

For examples of this approach actually working, one has to look back before the First World War, when the Gold Standard left no room for inflating away debt. Between 1896 and 1913, France shrank its debt-to-GDP ratio from 96% to 51% by consistently running budget surpluses.

The most successful case, however, was that of the United Kingdom after the Napoleonic Wars. Over the next nine decades, Britain maintained surpluses and brought its debt-to-GDP ratio down from 194% in 1822 to just 28% by 1913 — an extraordinary feat of fiscal restraint and steady economic growth.

In the context of history, it remains one of the most remarkable examples of a country genuinely growing its way out of debt, without default, inflation, or financial repression.

Still, I can’t help but wonder: should we give Britain full credit for this feat achieved in the 1800s?

After all, this was the height of its imperial power, when vast wealth flowed from colonies like my own homeland, India, into London’s coffers. Was that extraordinary debt reduction simply the product of fiscal discipline and productivity — or was it underwritten by the extraction, taxation, and plunder of colonial economies? In other words, did the people of India and other colonies end up paying the price for Britain’s debt addiction?

Someone always pays the bill. Who will it be this time?

That’s all for this week folks, see y’all next week.

Valuable historical summary - though centred on sovereign debt, the mechanisms of financial repression, inflation, and fiscal tightening align with themes of liquidity and operational risk TCLM covers. If you're modelling how macro policy impacts business finance, it’s worth a skim.

(It’s free)- https://tradecredit.substack.com/